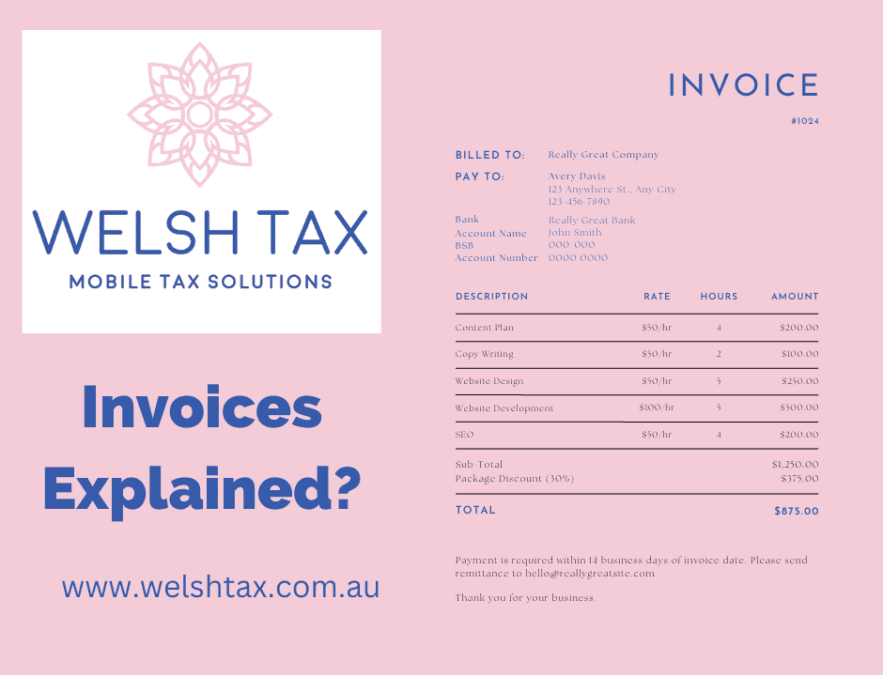

An invoice is a document that is time/date and itemises and records a transaction between a buyer and a seller. If goods or services were purchased on credit, the invoice usually specifies the terms of the transaction as well as information on the payment methods.

Accounting internal controls and audits rely heavily on invoices.

Invoices typically outline payment terms, unit costs, shipping and handling, and any other terms agreed upon during the transaction.

To be able to claim a tax deduction for item(s) purchased during the financial year you must hold a tax invoice.

As per the Australian Tax Office, all tax invoices for sales that are less than $1,000 must include the following details:

- Seller’s identity

- Seller’s Australian business number (ABN)

- Date the invoice was issued

- A brief description of the items sold, including the quantity (if applicable) and the price

- GST amount (if any) payable – this can be shown separately or, if the GST amount is exactly one-eleventh of the total price, as a statement which says ‘Total price includes GST’

- Extent to which each sale on the invoice is a taxable sale

For Items in excess of $1,000 the tax invoice will also include (the above items) plus the GST included in the price and the buyers identity including ABN.

If a tax invoice has both taxable and non- taxable sales, the tax invoice must clearly show which items are taxable and those that are input taxed or GST free.

If you didn’t receive an invoice on purchase of an item you are able to request a copy and the seller is required to supply this to you within 28 days.

Invoices should always be accurate, descriptive and timely. This is vital to ensuring you correctly claim your deductions and have proof of purchase.

If an invoice is issued on paper that will fade make sure you keep a photocopy. Invoices that are faded and unreadable will not be accepted by the ATO in the event of an audit.

Prepared with reference to www.ato.gov.au

More questions?

Follow us for more tips! https://www.facebook.com/Welshtax

Recent Comments