‘Tis the season of gifts & parties

But did you know that not all gifts & parties are equal when it comes to Taxes & GST?

If you are considering giving Christmas gifts or having a Christmas party, there are several things to consider.

If you are considering paying your employees a Christmas reward, please consider the below. Each employer situation may be different so please consult us to discuss your particular situation.

Tax Deductibility

Gifts can be categorised as Entertainment and Non-Entertainment.

Entertainment gifts include gifts such as theatre or movie tickets, sporting events, accommodation for holidays, flights, membership to a club or any similar items. These are not deductible for tax purposes and No GST can be claimed.

Non-entertainment gifts are deductible for income tax purposes. GST can also be claimed. Non-entertainment gifts may include gifts such as a Christmas hamper, bottles of wine or spirits, gift vouchers, flowers or other similar items. (please note most gift vouchers do not include GST)

These gifts should also be infrequent or irregular. If you wish to make a gift to your staff that the most beneficial to you as an employer is a a non-entertainment gift.

You do also need to consider Fringe Benefits Tax (FBT)

The provision of a gift to an employee at Christmas time may be considered a minor benefit. However, where the value of the gift is less than $300 these benefits are not subject to FBT.

Minor benefit conditions:

- Gifts are provided to staff or their associates (for example a spouse/family members),

- Gifts are provided on an “infrequent” or “irregular” basis, and

- the gift is not considered a reward for services.

The simplest and most beneficial to you as an employer (from a tax perspective) is a gift to your staff member which is a Non entertainment gift less than $300.

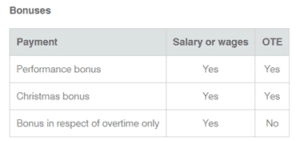

The other option to reward your staff member is a bonus which is tax deductible when paid and subject to PAYG Withholding tax, If the bonus is paid and is considered ordinary times earnings (OTE) superannuation guarantee (at the current rate) must also be paid on the gross amount.

We know it can be a little confusing, and as always, we’re here to answer any questions you might have. Please reach out if you need any further clarification, email us at [email protected] or call our office on 5494 9173.

Recent Comments